The union budget throws up surprises. At times, a punch. This time, it has thrown up a surprising punch. A new TDS (Tax deducted at source) section 194Q of the Income Tax Act. Allow us to explain it in simple terms and soften the blow for you!

A few businesses were hula hooping in a loophole in TCS (Tax collected at source) launched in 1 Oct 2020. The Indian Government has filled the hole and stopped people from playing with it. In enters section 194Q TDS on purchase of goods, effective from 1st July 2021. Simply put, 194 Q ensures every rupee remains in plain sight when a purchase or sale happens.

What is TDS on purchase of goods under Section 194Q?

From salary payment to rent, the Government collects tax in advance from assesses in the form of TDS. From 1st July 2021, TDS of 0.1% will have to be deducted by a buyer on purchase of goods, if the buyer has made a turnover of more than Rs. 10 crores in the preceding financial year and if the purchase from a particular seller (resident of India) goes above Rs. 50 lakhs in any preceding financial year.

The act also states that if PAN is not furnished by the recipient of income (seller), then TDS of 5% will be enforced.

How does TDS function under the new section?

Assume, Arvind Stores (AS) has had a turnover of more than Rs. 10 crores in the preceding financial year and purchases goods worth of Rs. 2,00,000 from Ashok Enterprises. The TDS deduction possibilities are:

Scenario 1: If AS had already purchased goods for Rs. 49 lakhs in the financial year, then TDS will be applicable for only Rs.1 lakh : (Rs. 49 L + Rs. 2 L) – Rs. 50 L = Rs. 1 L.

Scenario 2: If AS had already purchased goods for more than Rs. 50 Lakhs in the financial year, then TDS will be applicable on current purchase amount of Rs. 2 Lakhs.

Will TCS (Tax collected at source) be collected along with TDS?

Most sellers, whose turnover was less than Rs.10 crores and made a sale of Rs. 50 lakhs to a particular buyer in a financial year, were able to dodge the TCS punches till now, like ace boxer Mohammad Ali would.

While such businesses celebrated with fries (  ), the Government of India just got wise!

), the Government of India just got wise!

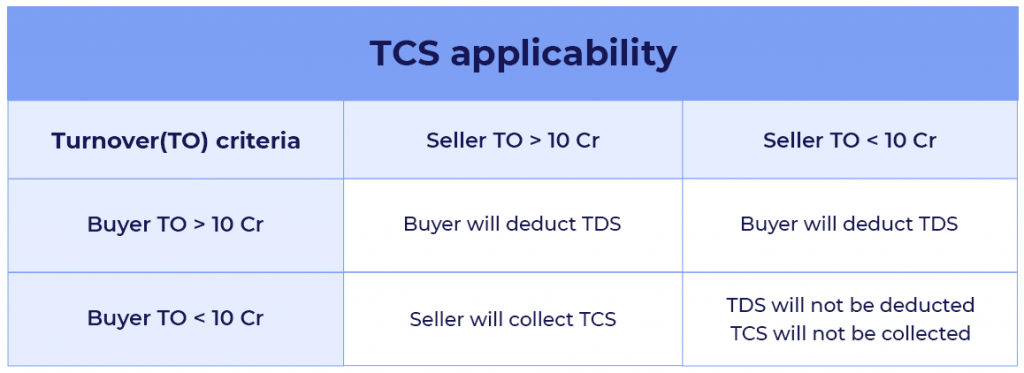

From 1st July 2021, any buyer (turnover>10 crores) will have to deduct TDS if the seller is not liable to collect TCS (turnover < Rs. 10 crores). Also, TCS will be collected by a seller only when the buyer is not liable to deduct TDS on purchase of goods (i.e.,) if the buyer’s turnover is less than Rs. 10 crores and purchases in the financial year go above 50 lakhs.

However, if the turnover of both the parties is less than Rs. 10 crores in the preceding FY then, neither TDS nor TCS will come into force.

How can Gofrugal help manage TDS?

We reach the climax of Section 194Q (TDS) and Section 206 C – 1 H (TCS). We presume you want a happy ending. Which means you should switch to smart tech’s side. If not, for the thousands of invoices that you make, you might end up:

1) Calculating TDS amount for each and every bill using a calculator.

2) Missing out TDS deduction at the time of purchase.

3) Passing hundreds of journal entries for TDS collected one by one. Even if you miss one TDS payment, then 30% of the expense shall be disallowed under section 40a (ia) of the Income Tax Act.

Relax, Gofrugal can guide you. From TDS calculations to passing a journal entry for TDS deducted will be taken care of. Even TDS deductions on other transactions like rent expense can be smartly managed.

Sounds good? All you need to do is to click the button below and register.