A business customer walks up to your counter, picks up a bulk order, and asks: "Can you give me a proper invoice with our GSTIN?" You hand over the usual printout from your POS system. They look at it and say, "This won't work for our accounts."

If that moment sounds familiar or if it hasn't happened yet but you sense it might, this blog is for you.

"Billing" and "invoicing" are used interchangeably across India's retail sector. Most billing software pages, product brochures, and even accountant conversations treat them as the same thing. For everyday B2C counter sales, that's mostly fine. But the moment GST compliance enters the picture when a registered business buyer needs to claim Input Tax Credit, when an e-invoicing mandate applies, or when an audit comes calling, the distinction between a bill and a tax invoice can have real financial consequences.

This blog draws a clear line between the two, explains exactly when each applies in a retail shop context, and shows why your billing software needs to handle both correctly without your team needing to think about it.

What is billing? (The process)

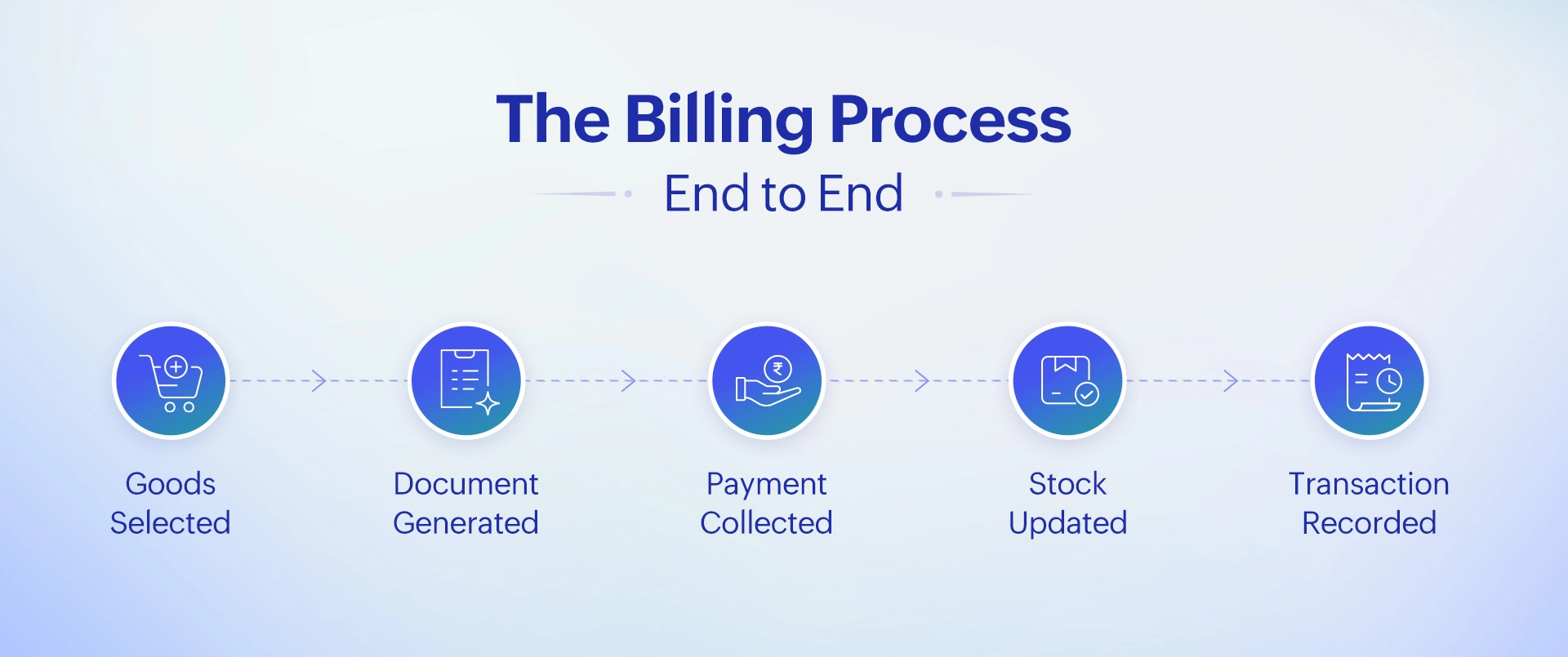

Billing is the complete, end-to-end process of charging a customer for goods or services. In a retail shop, it covers everything from the moment an item is scanned at the counter to the moment payment is received, the stock is updated, and the transaction is recorded in your accounts.

When a customer walks into a kirana store, picks up items, and pays at the counter, that's billing. When your POS system prints out a receipt, calculates GST, updates your inventory, and logs the sale, that's the billing process at work. The "bill" the customer receives is just one part of that process.

Think of billing as the system; the document it generates is one output of that system.

What is invoicing? (The document)

An invoice is a specific, formal document that requests payment and records a transaction in legally sufficient detail. It is one output of the billing process but it carries more weight than a standard retail bill.

In a retail context, invoicing becomes critical in three situations: when the buyer is a GST-registered business (B2B), when payment will happen after the goods are delivered (credit terms), or when the transaction requires a formal record for accounting, auditing, or ITC purposes.

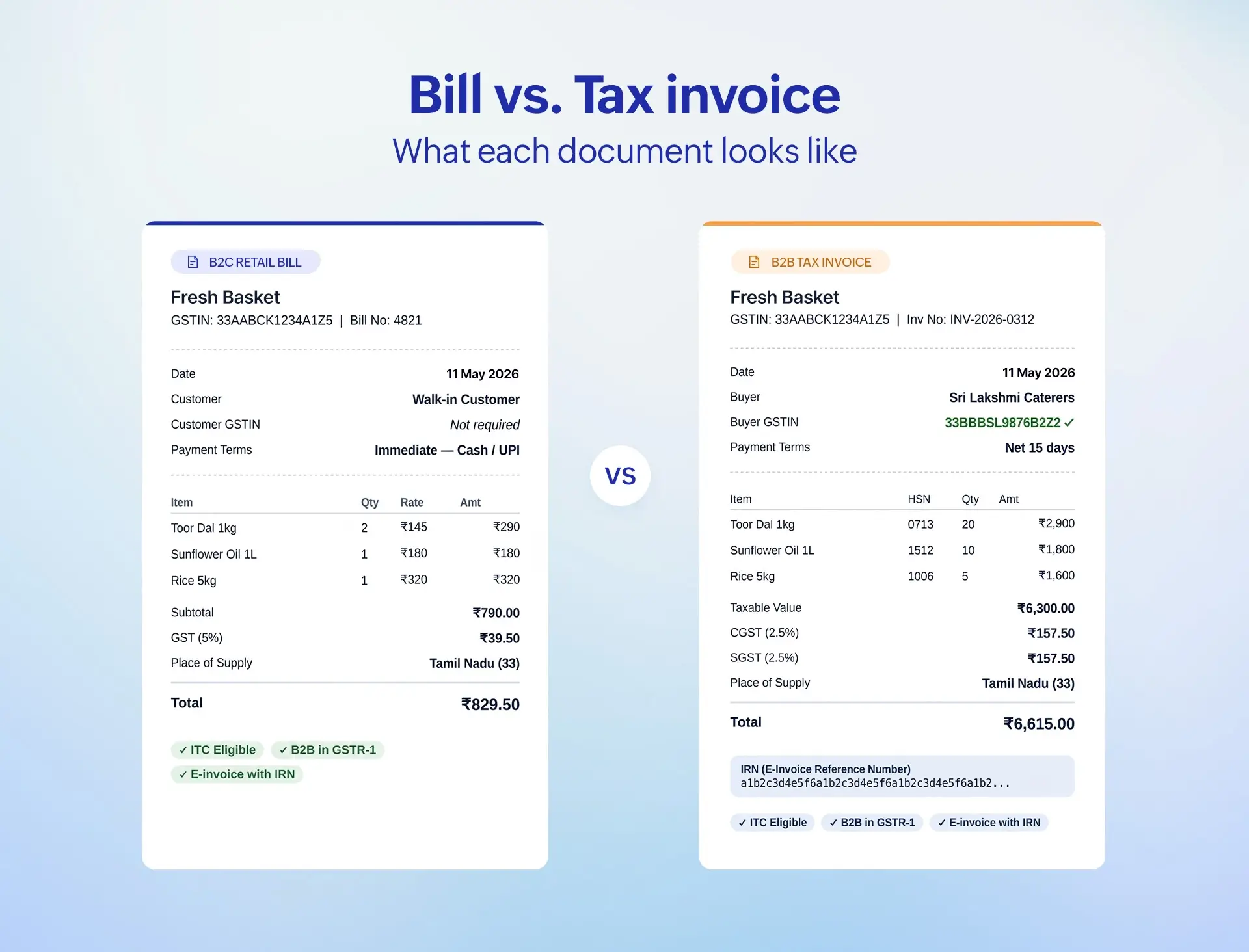

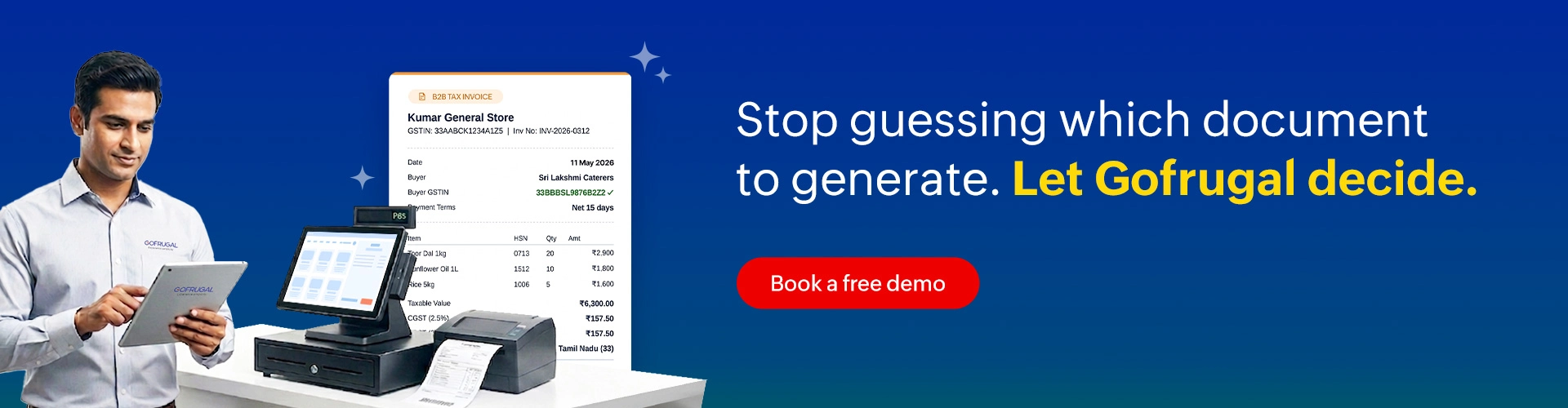

A GST tax invoice must include both the seller's and buyer's GSTIN, a unique invoice number, HSN codes, item-wise tax breakdowns (CGST/SGST or IGST), place of supply, and applicable payment terms. A standard retail bill for a walk-in consumer does not need all of this.

In short: every invoice is part of a billing process, but not every bill is an invoice.

Billing vs. Invoicing — Quick comparison

| Dimension | Bill (B2C Retail) | Tax Invoice (B2B) |

| Document purpose | Acknowledge the transaction; request immediate payment at the counter | Formally request payment with legally required GST details |

| Who receives it | B2C — walk-in consumer customer | B2B — GST-registered business buyer |

| Payment timing | Immediate, at the point of sale | Deferred — 7, 15, or 30 days as agreed |

| Is the GSTIN of the buyer required? | No | Yes — mandatory for ITC eligibility |

| Are HSN codes required? | Recommended; mandatory above certain thresholds | Mandatory |

| ITC eligibility for buyer | Not applicable — B2C end consumer | Yes — buyer can claim Input Tax Credit |

| How it's reported in GSTR-1 | Aggregate summary (B2CS/B2CL) | Invoice-wise detail |

| E-invoicing with IRN | Not mandatory (B2C pilot in progress) | Mandatory for sellers above ₹5 crore turnover |

Understanding the differences in detail

Purpose and document type

A retail bill acknowledges a completed transaction and records that payment was received, typically at the point of sale. It is designed for speed and simplicity. A tax invoice, by contrast, is a formal legal document under GST law. It creates an obligation (payment is due) and an entitlement (the buyer can use it to claim ITC). The document format, mandatory fields, and reporting obligations are all different.

Who the document is for

A bill is issued to an end consumer, an individual buying for personal use. Their GSTIN is not required because they are not in the GST input tax chain. A tax invoice is issued to a GST-registered business buyer who is part of that chain. Their GSTIN on the invoice is the link that allows them to claim credit for the tax they paid on that purchase. Without that link, the credit is lost.

Payment timing

Bills at retail counters are settled immediately with cash, card, or UPI at the point of sale. Invoices, especially in B2B trade, typically carry payment terms. A wholesale distributor delivering stock to a retailer, for example, will issue an invoice with a 15- or 30-day payment window. The invoice serves as the formal document governing that credit relationship.

GST compliance implications

This is where the distinction has the most direct business impact. Under GST, B2C transactions are reported in aggregate in GSTR-1 (under B2CS and B2CL categories). No ITC is available to the buyer. B2B transactions, however, must be reported invoice-by-invoice in GSTR-1, and the tax invoice is the document that enables the buyer to claim ITC in their own returns. If a B2B buyer receives a simple bill without their GSTIN and proper tax details, that purchase is invisible to their ITC claim, meaning they pay more tax than they should.

E-invoicing (2026 update)

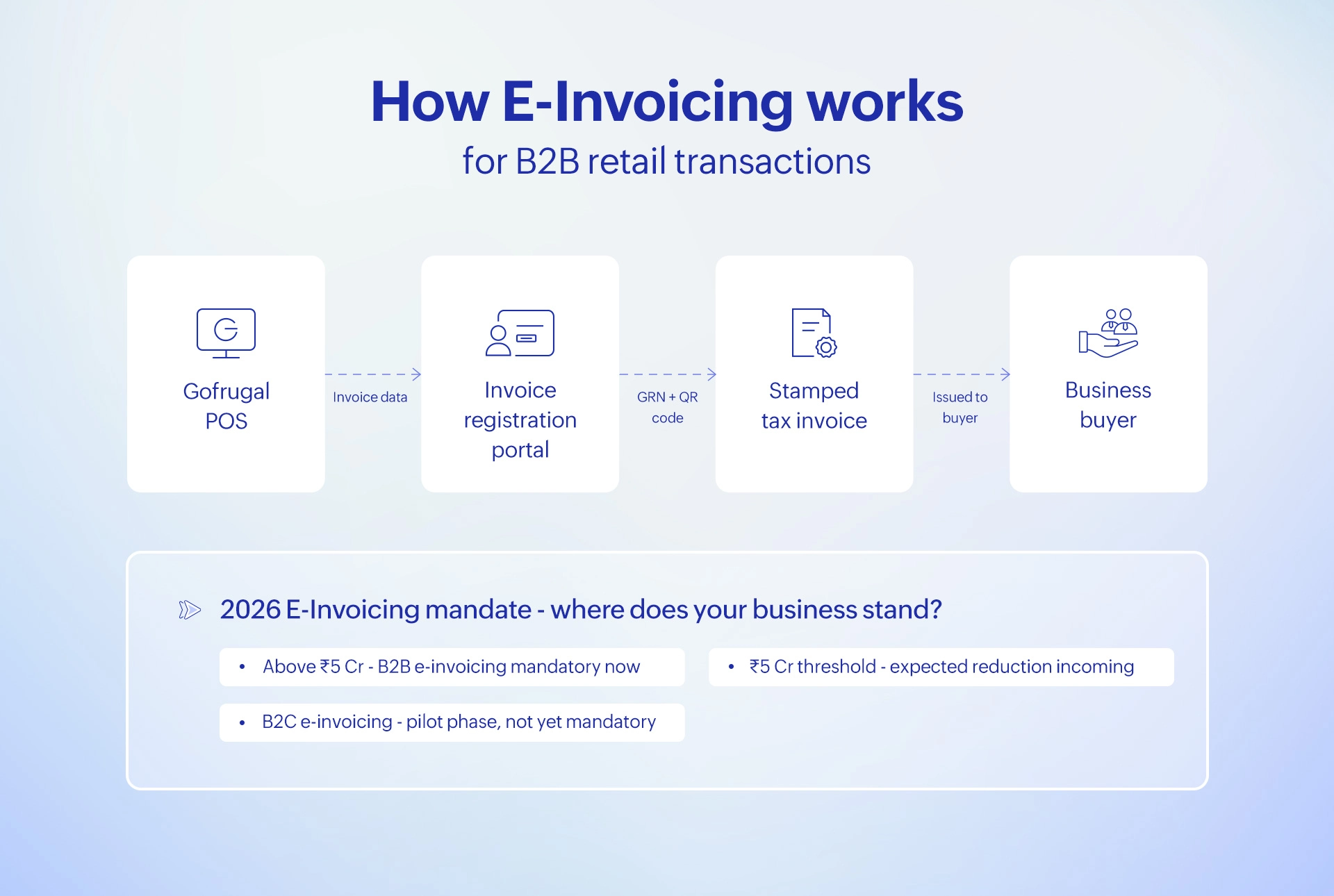

India's e-invoicing system adds another layer to this distinction. For B2B invoices issued by businesses with annual turnover above ₹5 crore, the invoice must be registered on the government's Invoice Registration Portal (IRP) to receive a unique Invoice Reference Number (IRN) and digitally signed QR code. This applies to B2B transactions only. B2C invoices are not currently subject to e-invoicing mandates, though a pilot is underway for high-turnover businesses. The e-invoicing threshold is expected to reduce further, making it relevant to a larger share of retail businesses.

When does the difference matter for your retail shop?

For most daily transactions, the distinction is invisible. A walk-in customer buys groceries, pays, and gets a receipt; billing and invoicing are the same thing at that moment. But there are four retail scenarios where the difference matters enormously.

Scenario 1: A registered business buys in bulk

A local restaurant owner comes to your wholesale outlet to buy provisions. They are GST-registered and will claim ITC on this purchase. If you give them a standard B2C bill without their GSTIN, they cannot claim that credit. They end up paying the full tax burden, which makes buying from you more expensive than buying from a supplier who issues proper invoices. Over time, this costs you the relationship.

Scenario 2: Credit sales to business buyers

You supply goods to a small retailer on 30-day credit. A verbal agreement or a simple handwritten note is not sufficient for their accounts or yours. A proper tax invoice, numbered and dated, with agreed payment terms, is the document both parties need for their books. It is also what their lender or auditor will ask for if they ever need to verify receivables.

Scenario 3: An audit or GST notice arrives

The GST department flags a mismatch between your GSTR-1 and a buyer's GSTR-2B. The buyer has claimed ITC against transactions that appear in your books only as B2C bill summaries, not as named invoices. The document trail matters. If your billing system was generating the wrong document type for B2B customers, reconciling that gap is costly and time-consuming.

Scenario 4: E-invoicing threshold is crossed

Your business grows and crosses the ₹5 crore annual turnover threshold. From that point, every B2B invoice you issue must be registered on the IRP and carry an IRN. If your billing software does not support e-invoice generation natively, you now have a compliance gap that affects every customer you serve.

The GST angle — Why this distinction is compliance-critical in 2026

India's GST framework treats B2B and B2C transactions fundamentally differently. Understanding this is not just useful for accountants, it has direct operational implications for any retail business that sells to both consumers and registered business buyers.

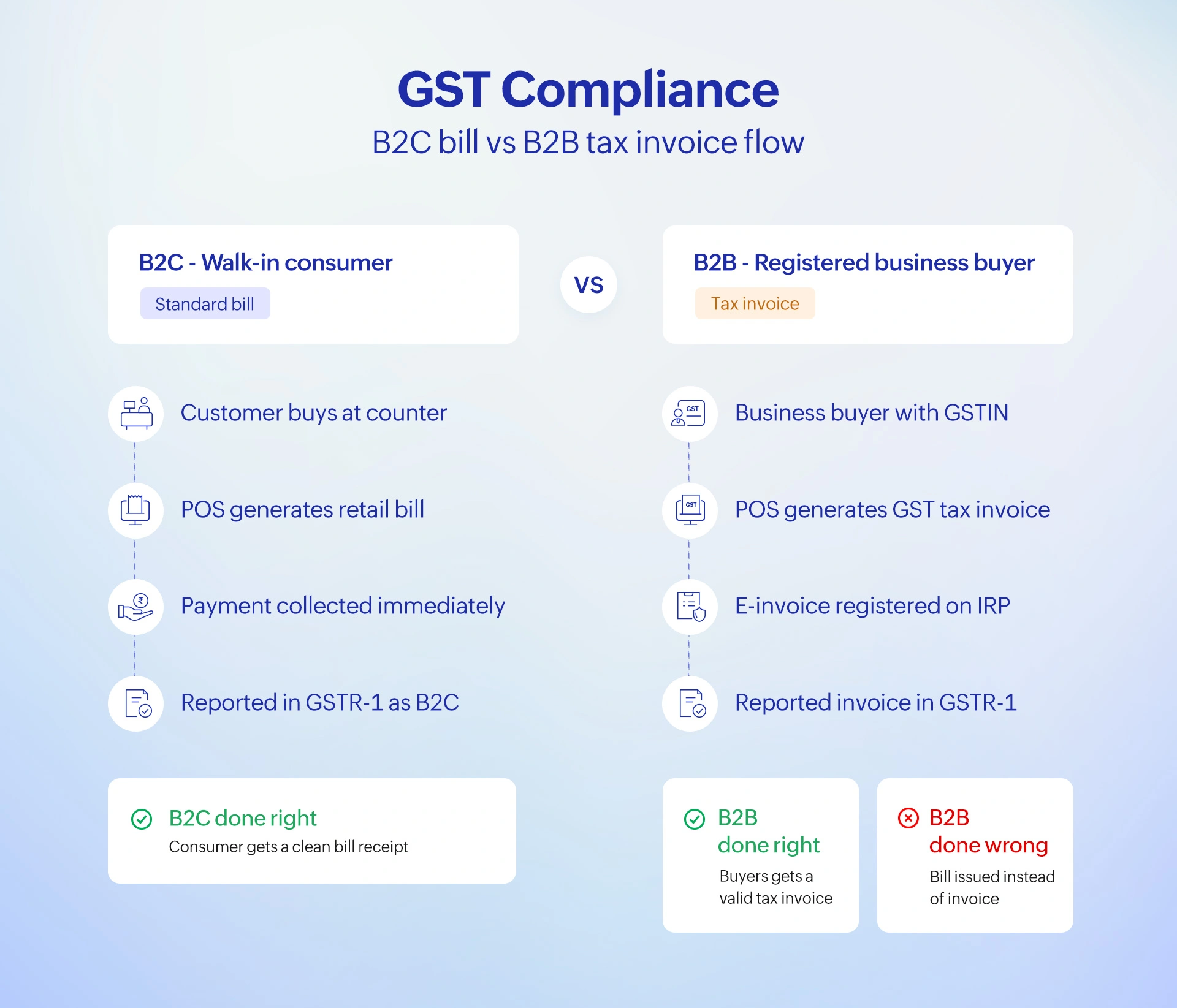

For B2C transactions, the seller reports aggregate turnover figures in GSTR-1. The consumer does not need to file any matching return. There is no ITC in play. A standard POS-generated bill satisfies the compliance requirement.

For B2B transactions, the rules are stricter. Every invoice must be reported individually in GSTR-1, with the invoice number, date, buyer's GSTIN, taxable value, and tax breakdowns. The buyer reconciles these details in their own GSTR-2B. Any mismatch, including a missing or incorrect GSTIN, can block their ITC claim and trigger a notice.

E-invoicing raises the stakes further. For businesses above ₹5 crore annual turnover, B2B invoices must be uploaded to the Invoice Registration Portal before they are issued to the buyer. The IRP returns an IRN, a unique identifier and a digitally signed QR code that must appear on the invoice. An invoice issued without an IRN is not a valid tax invoice for ITC purposes, regardless of how accurate the other details are.

The B2C e-invoicing pilot, requiring dynamic QR codes for consumer-facing invoices from high-turnover businesses, signals that compliance requirements for B2C transactions are also set to tighten. Staying ahead of this curve means having billing software that is already built for both.

Does your billing software handle both? Here's a checklist

Most retail billing software is built for one scenario: the B2C counter sale. When a business buyer walks in, the gap becomes visible. Here is what your billing software should do without any manual intervention:

- Detect whether the transaction is B2C (consumer) or B2B (registered business buyer) based on GSTIN input.

- Automatically generate a standard retail bill for B2C transactions—no unnecessary fields, fast checkout.

- Switch to a full GST tax invoice format for B2B transactions including buyer GSTIN, HSN codes, CGST/SGST/IGST breakdowns, and place of supply.

- Generate e-invoices with IRN and QR code for qualifying B2B transactions without leaving the billing counter.

- Manage credit notes correctly for both transaction types with proper GST reversal for B2B.

- Report B2C and B2B transactions in the correct GSTR-1 categories automatically.

If your current system requires manual switching, separate tools for B2B invoicing, or manual uploads for e-invoicing, you are adding compliance risk and operational overhead that should not exist.

How Gofrugal handles billing and invoicing for retail shops

Gofrugal's retail POS is built to handle both billing and invoicing from the same counter, for every customer type, without manual intervention.

Automatic B2B/B2C detection

When a customer's GSTIN is entered at the billing counter, Gofrugal automatically switches to a GST-compliant tax invoice format with all mandatory fields populated. For walk-in consumers, the standard POS bill format is used. Your billing team does not need to know the compliance rules; the system handles it.

GST tax invoice generation

For B2B transactions, Gofrugal generates invoices that include both parties' GSTINs, HSN codes, item-wise tax breakdowns, place of supply, and a unique invoice number series, all fields required for ITC eligibility. The invoice is GSTN-compliant out of the box.

E-invoice with IRN

For businesses above the e-invoicing threshold, Gofrugal integrates with the Invoice Registration Portal to generate IRNs and digitally signed QR codes in real time from the same billing counter—no separate upload, no third-party tool, no manual step.

Credit note management

Returns and price corrections are handled correctly for both transaction types. B2B credit notes reference the original invoice and update GSTR-1 accordingly, allowing the buyer to reverse their ITC claim. B2C refunds are processed without affecting the ITC chain.

GSTR-1 reporting

Gofrugal auto-categorises transactions as B2CS, B2CL, or B2B in your GSTR-1 data, so your return filings reflect the correct document types for every sale without any manual sorting.

Billing and invoicing are not the same thing. Even though most retail software, and most retail conversations, treat them as if they are. The distinction is invisible in a B2C counter sale. It becomes critical the moment a registered business walks in, asks for a proper tax invoice, or expects to claim ITC on their purchase.

Getting this right is not about adding complexity to your operations. It is about having a system that makes the right decision automatically. It is one that issues the correct document for every customer type, handles e-invoicing with IRN when required, keeps your GSTR-1 clean, and never puts your B2B buyers in a position where their tax credit is at risk.

Gofrugal handles billing and invoicing for every retail scenario—from the kirana counter to the wholesale floor—in a single system, without manual switching or compliance guesswork.

Frequently asked questions

What is the difference between billing and invoicing?

Billing is the end-to-end process of charging a customer. It includes generating the document, collecting payment, and recording the transaction. Invoicing refers specifically to the formal document that requests payment. In practice, billing is the process; an invoice is one of its outputs. For most retail counter sales, a bill or receipt is sufficient. A formal invoice becomes necessary when selling to a registered business buyer or when payment will be made at a future date.

Is a bill the same as an invoice?

Not exactly. A bill is typically issued for immediate payment in consumer transactions like a grocery receipt or a restaurant bill. An invoice is a formal document issued for deferred payment or to a business buyer, and includes additional details like payment terms and the buyer's GSTIN. The same document can be called an invoice by the seller and a bill by the buyer but in GST compliance terms, they have different requirements.

When should a retail shop issue a tax invoice instead of a simple bill?

A retail shop must issue a proper GST tax invoice, not just a simple bill, when the buyer is a GST-registered business and wants to claim Input Tax Credit (ITC). In this case, the invoice must include the buyer's GSTIN, full item-wise tax breakdowns, HSN codes, and the place of supply. If the buyer is an individual consumer, a standard POS-generated bill is sufficient.

Does a retail shop need to give GST invoices to all customers?

No! For walk-in consumer customers (B2C transactions), a standard retail bill with GST details is sufficient, the buyer's GSTIN is not required. A full GST tax invoice is required only when the buyer is a GST-registered business (B2B transaction) who needs to claim ITC. Getting this wrong means the business buyer cannot claim their tax credit, which can damage the supplier relationship.

What is e-invoicing and does it apply to retail shops in India?

E-invoicing is the process of registering a B2B invoice on the government's Invoice Registration Portal (IRP) to receive a unique Invoice Reference Number (IRN) and QR code. As of 2026, e-invoicing is mandatory for all businesses with annual turnover above ₹5 crore for B2B transactions. It does not currently apply to B2C retail transactions, though a pilot is being planned. Retail shops selling to other businesses must generate e-invoices with IRN for those qualifying transactions.

Can the same billing software handle both billing and invoicing?

Yes and for most retail shops, it should. Good retail billing software automatically detects whether a transaction is B2C (standard bill) or B2B (tax invoice with GSTIN), generates the correct document, and handles e-invoice generation with IRN for qualifying transactions. Gofrugal's POS does this from the same billing counter without any manual switching between document types.

What happens if a retail shop issues a bill instead of an invoice to a B2B customer?

If a business customer receives a simple bill without their GSTIN and proper tax invoice details, they cannot claim Input Tax Credit on that purchase. This means they pay more tax than they should, which makes your shop a less attractive supplier than competitors who issue proper invoices. It can also create GST reconciliation issues for both parties during return filing.

What is the difference between a bill and an invoice in GST India?

Under GST, a tax invoice is the formal document required for B2B transactions. It must include both parties' GSTINs, HSN codes, tax breakdowns, and is reported invoice-wise in GSTR-1. A bill of supply or simplified invoice is used for B2C transactions, where the consumer's GSTIN is not required and summaries are reported in aggregate in GSTR-1. The key difference is the ITC chain: only transactions backed by a proper tax invoice allow the buyer to claim input tax credit.

What details must a GST tax invoice include that a simple bill does not?

A GST tax invoice must include the supplier's and buyer's GSTIN, a unique invoice number, date, description of goods with HSN codes, taxable value, applicable GST rate, and CGST/SGST/IGST breakdowns by line item, and place of supply. A simple retail bill for a consumer typically shows only items, prices, total GST charged, and payment details. It does not need the buyer's GSTIN or itemized tax type breakdowns.

Is billing software the same as invoicing software for retail?

In practice, for retail, the best systems do both. "Billing software" typically refers to POS-based counter sales systems, while "invoicing software" often refers to tools that generate formal invoices for B2B or deferred-payment transactions. Modern retail billing software like Gofrugal handles both from the same interface: POS billing for walk-in customers and formal tax invoice generation for business buyers, including e-invoice registration with IRN.

What is a credit note and when does a retail shop need to issue one?

A credit note is a document issued by a seller to reverse or partially reduce a previous invoice or bill, typically in case of returns, price corrections, or cancelled orders. In GST terms, B2B credit notes must reference the original invoice and be reported in GSTR-1, adjusting the seller's output tax and allowing the buyer to reverse their ITC claim. For B2C transactions, returns are usually handled as refunds or adjustments.

Does the billing versus invoicing distinction matter for small kiranas?

For a kirana that sells only to individual consumers, the distinction rarely matters in daily operations, a standard bill is sufficient for every transaction. It becomes relevant the moment a small business owner (a caterer, a restaurant, a local retailer) starts buying regularly and asks for proper invoices with their GSTIN. As the business grows and more B2B buyers come in, having billing software that handles both becomes not just convenient but compliance-critical.